Every business that holds stock has to answer one deceptively simple question: what did this inventory actually cost us? The answer determines your cost of goods sold, your reported profit, your tax liability, and the value sitting on your balance sheet. Get it wrong, and you could be overpaying tax, understating losses, or making pricing decisions based on numbers that don’t reflect reality.

This is where the FIFO vs LIFO vs weighted average debate comes in. These are the three most widely used inventory valuation methods, and choosing between them isn’t just an accounting formality. It directly shapes how your business measures profitability and manages stock. If you’re running a warehouse or scaling an inventory management system, understanding these methods is foundational to getting your numbers right.

In this guide, we’ll break down how FIFO, LIFO, and Weighted Average Cost work, walk through real calculations, explain what Indian accounting standards actually permit, and help you figure out which method fits your business.

What Is Inventory Valuation and Why It Matters

Inventory valuation is the accounting process of assigning a monetary value to the stock a business holds at any given point: raw materials, work-in-progress, or finished goods. Since prices of raw materials and purchased goods change over time, the same physical unit of stock can have different costs depending on when it was bought.

Inventory valuation matters for three practical reasons:

- Cost of Goods Sold (COGS) accuracy: Your valuation method directly decides how much cost gets matched against revenue in a given period, which in turn affects gross profit.

- Tax liability: Since profit is taxed, the valuation method chosen changes how much tax a business pays in a given year.

- Balance sheet accuracy: Inventory is a current asset, and its reported value affects working capital calculations, loan eligibility, and investor confidence.

Valuation is closely tied to broader inventory control types, methods, and strategies. You can’t manage stock effectively if you don’t know what it’s actually worth. Let’s look at the three methods in detail.

FIFO vs LIFO vs Weighted Average: Quick Comparison

Before diving into each method individually, here’s a snapshot comparison:

| Factor | FIFO | LIFO | Weighted Average |

|---|---|---|---|

| Assumption | Oldest stock sold first | Newest stock sold first | All stock costed at average rate |

| Best during inflation | Higher profit, higher tax | Lower profit, lower tax | Smooths out price swings |

| Allowed in India (AS 2 / Ind AS 2) | Yes | Not for tax reporting | Yes |

| Matches physical stock flow | Usually yes | Usually no | Not applicable |

| Best suited for | Perishables, FMCG, fashion | Non-perishable, bulk commodities (restricted in India) | Homogeneous, mixed-batch inventory |

| Complexity | Low to moderate | Moderate | Low |

Now let’s unpack each one.

FIFO (First-In, First-Out) Explained

FIFO assumes that the oldest inventory in stock is the first to be sold or used. In other words, the cost of the earliest purchased goods is recognized first in your cost of goods sold, while the most recently purchased stock remains valued in your closing inventory.

FIFO Formula and Example

The logic is straightforward: cost of goods sold = cost of the oldest units in stock, in the order they were purchased.

Example: A distributor buys inventory in two batches:

- Batch 1: 100 units at ₹200 each = ₹20,000

- Batch 2: 100 units at ₹240 each = ₹24,000

If the business sells 120 units, under FIFO:

- 100 units are costed from Batch 1 at ₹200 = ₹20,000

- 20 units are costed from Batch 2 at ₹240 = ₹4,800

- Total COGS = ₹24,800

- Remaining inventory (80 units from Batch 2) = ₹19,200

Why Businesses Choose FIFO

FIFO tends to mirror the actual physical movement of stock in most warehouses. You generally want to move older stock out before it expires, becomes obsolete, or gets damaged. This makes it a natural fit for businesses managing perishable goods, where batch and expiry tracking is critical to compliance and safety.

FIFO is well suited to:

- FMCG and food businesses with expiry-driven stock rotation

- Fashion and seasonal retail, where older styles need to move first

- Businesses with rising prices, since it results in inventory value on the balance sheet reflecting more recent (and therefore more current) costs

- Companies seeking simpler compliance, since FIFO is accepted under nearly every accounting framework globally, including Ind AS 2 and IFRS

The tradeoff: during inflationary periods, FIFO matches older, cheaper costs against current revenue, which inflates reported profit, and therefore inflates the tax bill.

LIFO (Last-In, First-Out) Explained

LIFO assumes the opposite: the most recently purchased inventory is the first to be sold, while older stock remains in the warehouse on paper. This means the cost of goods sold reflects current (often higher) prices, while inventory on the balance sheet is valued at older, lower costs.

LIFO Formula and Example

Using the same batches as above (100 units at ₹200, 100 units at ₹240), if the business sells 120 units under LIFO:

- 100 units are costed from Batch 2 at ₹240 = ₹24,000

- 20 units are costed from Batch 1 at ₹200 = ₹4,000

- Total COGS = ₹28,000

- Remaining inventory (80 units from Batch 1) = ₹16,000

Notice how COGS is higher and closing inventory value is lower compared to FIFO. This is the core effect of LIFO during rising prices.

The India-Specific LIFO Restriction

This is where LIFO becomes tricky for Indian businesses. While Accounting Standard AS 2 technically permits LIFO in limited accounting contexts, Ind AS 2 (aligned with IFRS) does not allow LIFO for financial reporting, and Indian tax law does not recognize LIFO for computing taxable income. In practice, this means most Indian companies that might otherwise benefit from LIFO’s tax advantages have to convert to FIFO or Weighted Average for statutory reporting and tax filing.

This restriction is a critical point businesses often overlook when comparing FIFO vs LIFO vs weighted average purely from a theoretical standpoint: the “best” method on paper isn’t always the legally usable one in India. Because of this, LIFO sees very limited real-world adoption among Indian businesses, and it’s rarely a practical option unless a company has significant US operations where LIFO is permitted under GAAP.

Automate FIFO, LIFO & Weighted Average valuation

See how our Warehouse Management System handles inventory valuation for you — live.

Weighted Average Cost (WAC) Method Explained

The Weighted Average Cost method takes a different approach entirely. Instead of tracking which specific batch a unit came from, it calculates a single average cost per unit across all inventory available for sale, and recalculates this average every time new stock is purchased.

WAC Formula and Example

Formula: Weighted Average Cost per unit = Total cost of goods available for sale ÷ Total units available for sale

Using the same example:

- Batch 1: 100 units at ₹200 = ₹20,000

- Batch 2: 100 units at ₹240 = ₹24,000

- Total cost = ₹44,000, Total units = 200

- Weighted average cost per unit = ₹44,000 ÷ 200 = ₹220

If the business sells 120 units under WAC:

- COGS = 120 × ₹220 = ₹26,400

- Remaining inventory (80 units) = 80 × ₹220 = ₹17,600

Notice this sits neatly between the FIFO and LIFO results, which is exactly the point of averaging.

Why Businesses Choose Weighted Average

WAC is popular because it’s simple to implement, especially in systems where individual batches get physically mixed together (think grain, liquids, chemicals, or bulk hardware) and tracking which specific unit came from which purchase isn’t practical. It also smooths out short-term price volatility, which can make inventory turnover ratio calculations and margin analysis more stable and easier to interpret month over month.

WAC works well for:

- Manufacturing operations where raw materials from different purchases get combined into production batches

- Businesses with fluctuating supplier prices who want to avoid large swings in reported COGS

- Companies prioritizing simplicity in bookkeeping and lower administrative overhead

- Retailers selling commoditized, non-perishable goods where exact batch tracking isn’t essential

The tradeoff: because it averages out cost fluctuations, WAC can obscure real cost trends, which may lead to less precise pricing decisions if raw material costs are rising or falling sharply.

Impact on Profit, Tax, and Balance Sheet: A Side-by-Side Look

Using the numbers from our examples above (selling 120 out of 200 units, prices rising from ₹200 to ₹240), here’s how the three methods compare on financial outcomes:

| Metric | FIFO | LIFO | Weighted Average |

|---|---|---|---|

| COGS | ₹24,800 | ₹28,000 | ₹26,400 |

| Closing inventory value | ₹19,200 | ₹16,000 | ₹17,600 |

| Reported profit (higher COGS = lower profit) | Highest | Lowest | Middle |

| Tax impact | Higher (in rising price environment) | Lower (not usable for Indian tax purposes) | Moderate |

This table makes the practical stakes clear: the same underlying transactions produce three different profit figures purely based on the valuation method chosen. This is exactly why common inventory management challenges so often trace back to inconsistent or poorly understood valuation practices rather than the physical handling of stock itself.

Legal and Accounting Framework in India

For Indian businesses, the choice isn’t purely about strategy. It’s bounded by regulation. Here’s what governs inventory valuation in India:

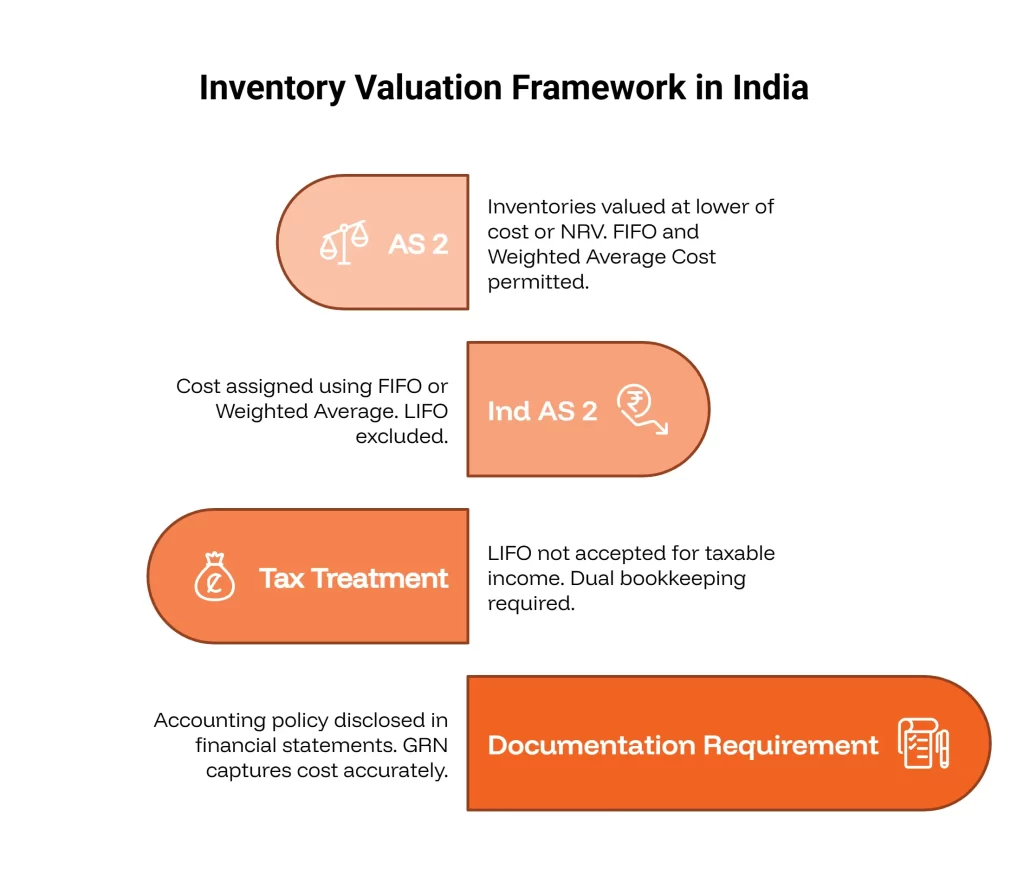

AS 2 (Valuation of Inventories): Under the Companies (Accounting Standards) Rules, AS 2 requires inventories to be valued at the lower of cost or net realizable value (NRV). It permits FIFO and Weighted Average Cost as the standard formulas for assigning cost, along with the Specific Identification Method (SIM) for inventory that isn’t ordinarily interchangeable, such as goods made for a specific customer project.

Ind AS 2: For companies following Indian Accounting Standards (mandatory for larger companies and listed entities), the same principle applies: cost must be assigned using FIFO or Weighted Average. LIFO is explicitly excluded, aligning India with IFRS globally.

Tax treatment: Since LIFO isn’t accepted for computing taxable income in India, companies that might use LIFO for internal management reporting still need to maintain FIFO or WAC-based records for GST and income tax filings. This dual bookkeeping requirement is one reason most Indian businesses simply standardize on FIFO or WAC across the board rather than maintaining separate systems.

Documentation requirement: Whichever method is chosen, the accounting policy must be disclosed in financial statements, along with the classification of inventory (raw materials, WIP, finished goods) and any write-downs recognized during the period. Getting this right starts at the point of purchase: every unit’s cost needs to be captured accurately on the Goods Received Note (GRN) so that whichever valuation method you use downstream has clean data to work with.

How to Choose the Right Method for Your Business

There’s no universally “best” method. The right choice depends on your industry, price environment, and operational setup. Here’s a practical way to think about it:

Choose FIFO if:

- You sell perishable goods, pharmaceuticals, or anything with expiry dates

- Your industry involves fast-moving, seasonal, or fashion-driven stock

- You want your reported inventory value to closely reflect current market costs

- You’re building financial statements for investors who prefer a method that shows stronger near-term profitability

Choose Weighted Average if:

- Your raw materials or stock get physically mixed and batch-level tracking isn’t feasible

- You want simpler, more stable accounting with fewer sharp swings in reported margins

- Your supplier prices fluctuate frequently and you’d rather smooth out the noise

- You’re a smaller business without the systems to track batch-level costs precisely

LIFO is rarely the right call for Indian businesses, given the tax and Ind AS restrictions. It’s generally only relevant for multinational businesses that also report under US GAAP.

Beyond the method itself, the “right” choice often depends on how disciplined your broader inventory practices are. Businesses that struggle with basic common inventory management challenges tend to see valuation errors compound regardless of which formula they pick, since the method is only as reliable as the data feeding it.

The Role of a WMS in Accurate Inventory Valuation

Manually tracking batch costs, purchase dates, and running average calculations across thousands of SKUs is where most businesses run into trouble. A warehouse management system automates this by tagging every incoming batch with its purchase cost and date, then applying your chosen valuation method consistently across every transaction, with no manual recalculation and no spreadsheet errors.

This becomes especially important when a WMS is integrated with your ERP and accounting system, since valuation data needs to flow accurately into financial statements without manual re-entry. A well-integrated system ensures that when stock moves, gets sold, or gets written off, the correct cost is pulled automatically based on your configured method: FIFO, WAC, or (where applicable) specific identification.

For growing businesses still relying on manual spreadsheets or basic registers, this is often the single biggest source of valuation errors: batches get mixed up, purchase costs get entered incorrectly, or average costs simply aren’t recalculated often enough to stay accurate.

Common Mistakes in Inventory Valuation

Even with a clear method chosen, execution often goes wrong. Some of the most frequent issues include:

Inconsistent application across periods: Switching valuation methods between financial years without proper disclosure creates compliance risk and makes year-over-year comparisons meaningless.

Poor data capture at receiving: If purchase costs aren’t logged accurately when stock arrives, every downstream valuation calculation, regardless of method, will be wrong. This is a recurring theme among the most costly inventory management mistakes businesses make.

Ignoring net realizable value: AS 2 requires inventory to be valued at the lower of cost or NRV, but businesses sometimes value stock purely on cost, overstating asset value when market prices have dropped or goods have become obsolete.

No reconciliation between physical and book stock: Valuation figures mean little if the underlying quantities are wrong. Regular inventory audits are essential to confirm that what’s recorded in the system matches what’s physically on the shelf.

Not prioritizing high-value SKUs: Not every item needs the same level of valuation scrutiny. Applying ABC analysis to identify your highest-value inventory lets you focus tighter valuation controls where the financial impact of an error is greatest.

FAQs on FIFO vs LIFO vs Weighted Average

No. While AS 2 technically references LIFO in limited contexts, Ind AS 2 excludes it entirely, and Indian tax law does not accept LIFO-based figures for computing taxable income. Businesses must use FIFO or Weighted Average for statutory and tax reporting.

Weighted Average is often easiest for small businesses due to its simplicity and lower administrative burden, especially when inventory tracking systems are still basic. FIFO is a close second, particularly for businesses selling perishable or fast-moving goods.

During inflation, FIFO results in higher reported profit and higher tax liability, because older, cheaper costs are matched against current revenue. LIFO does the opposite, reporting lower profit and lower tax, but as noted, this isn’t usable in India for tax purposes.

Yes, but the change must be justified, consistently applied going forward, and disclosed in financial statements as required under AS 2 and Ind AS 2. Frequent switching without valid reason raises compliance concerns.

FIFO tracks costs based on the actual sequence of purchases, while Weighted Average blends all costs into a single per-unit rate. FIFO better reflects physical stock movement; Weighted Average better handles inventory that’s physically mixed or difficult to track batch-by-batch.

Conclusion

The FIFO vs LIFO vs weighted average decision isn’t just an accounting technicality. It shapes your reported profit, your tax exposure, and the accuracy of your balance sheet. For most Indian businesses, the real choice comes down to FIFO versus Weighted Average, since LIFO’s tax and Ind AS restrictions make it impractical outside a narrow set of multinational cases.

FIFO suits businesses with perishable, seasonal, or fast-moving stock where physical flow naturally matches the accounting assumption. Weighted Average suits businesses with mixed-batch inventory or those prioritizing simpler, more stable bookkeeping. Whichever you choose, the accuracy of the underlying data (accurate purchase costs, disciplined stock counts, and a system that applies the method consistently) matters just as much as the method itself.

Getting inventory valuation right starts with getting the fundamentals of your inventory system right, whether that means moving off spreadsheets with automated processes or simply tightening how costs are captured at every stage, from receiving to dispatch. Either way, it takes the guesswork out of FIFO vs LIFO vs weighted average and ensures your financial statements reflect reality, not approximation.

Kapil Pathak is a Senior Digital Marketing Executive with over four years of experience specializing in the logistics and supply chain industry. His expertise spans digital strategy, search engine optimization (SEO), search engine marketing (SEM), and multi-channel campaign management. He has a proven track record of developing initiatives that increase brand visibility, generate qualified leads, and drive growth for D2C & B2B technology companies.